Voices

The Middle Corridor Is the Caucasus's Real Growth Story - and It's Still Under-Built

June 28, 2026

6

Min

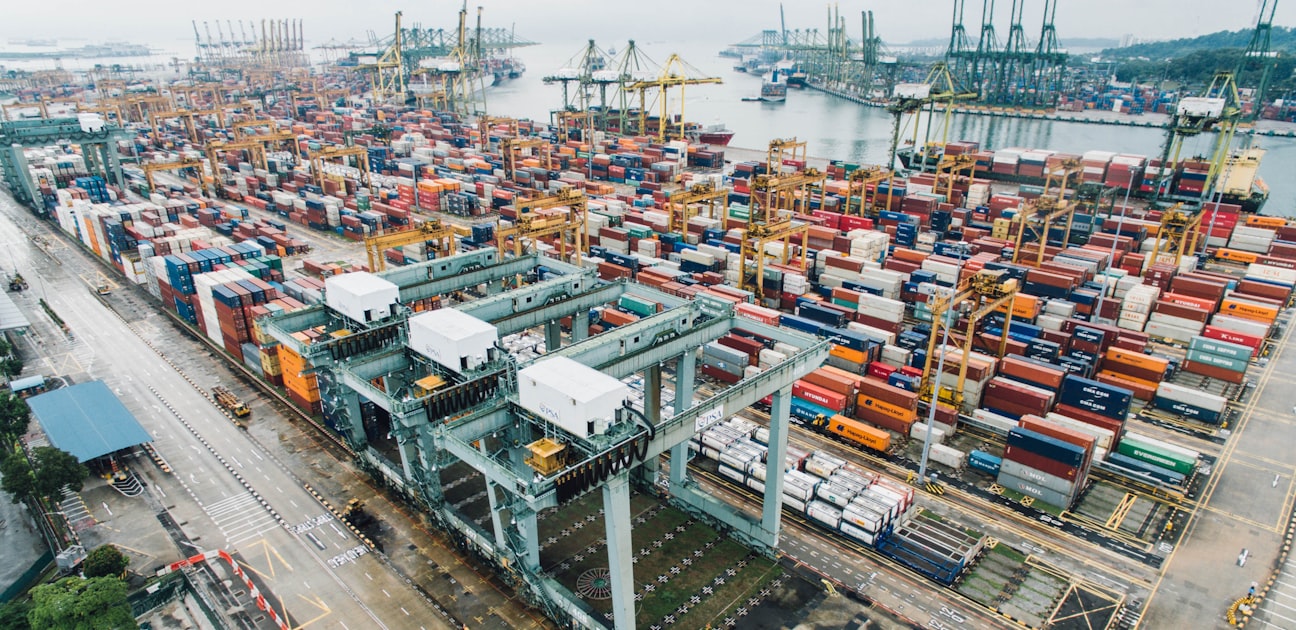

Containers and freight rail at a Caspian port - the choke points of the Middle Corridor sit at the water's edge, not on the map. Photo: Unsplash.

Every few months a new map circulates in Tbilisi, Baku and Brussels showing a thick line running from China across Kazakhstan, over the Caspian, through Azerbaijan and Georgia, and on to Europe. The line is the Middle Corridor, and the enthusiasm around it is, for once, justified by the numbers. Cargo across the Trans-Caspian International Transport Route has grown roughly fivefold in seven years. In the first quarter of 2026, container trains transiting Kazakhstan along the route rose 34 percent year on year, and total volumes crossed five million tonnes in 2025. When traffic through the Strait of Hormuz seized up earlier this year, weekly demand for Middle Corridor container slots spiked by several hundred percent almost overnight.

This is the South Caucasus's most important economic story - bigger than any single gas deal, more durable than any peace summit. It is also, on present trajectory, an opportunity the region is at real risk of under-building.

Start with why the demand is real and not a fad. The Northern Corridor through Russia is politically radioactive for Western shippers; the southern sea lanes through Hormuz and the Red Sea are physically dangerous. That leaves one route across the Eurasian landmass that touches neither Russian territory nor a contested chokepoint. Capital has noticed. European and international institutions have pledged on the order of roughly 10 billion dollars toward the corridor, the EU's Global Gateway commitment to Central Asia and the Caucasus has swelled past 20 billion euros, and in early 2026 the World Bank approved an 846-million-dollar guarantee backing 1.4 billion in financing for Kazakhstan's national railway. Money is not the constraint.

Here is the uncomfortable part. The corridor's binding bottleneck is not in the boardroom or the budget. It is physical, and it sits squarely on the territory of the two Caucasus states that stand to gain most. The Caspian is a landlocked sea with too few ships. The shortage of roll-on/roll-off and container vessels is the single hardest operational limit, and it cannot be fixed by laying more rail. Kazakhstan's railway only announced in 2026 that it would build its own fleet, starting with six vessels - a programme still early enough that much of it remains at feasibility stage. Worse, the sea itself is shrinking: water levels have been falling by up to 30 centimetres a year, cutting ferry tank-car traffic on the Baku-Kuryk route by more than a fifth. You cannot dredge your way out of a disappearing sea.

The Georgian end is no healthier. Existing Black Sea port capacity is close to exhausted, and the one project that would relieve it - the deepwater port at Anaklia - remains stalled. Tbilisi cut Anaklia's 2026 budget line from 150 million lari to 50 million, a telling signal of either fiscal caution or political ambivalence. A corridor is only as fast as its slowest node, and right now the slow nodes are a port that isn't being built and a sea that isn't being crossed at scale.

The honest counter-argument deserves a hearing. Carnegie's Temur Umarov argued this spring that the Middle Corridor still moves only about six percent of the Northern Corridor's hundred-million-tonne capacity, and that growth rates flatter a route that remains, in absolute terms, marginal. He is right about the arithmetic. But the conclusion does not follow. Marginal routes become structural ones precisely when the alternatives close - and in 2026 the alternatives are closing faster than the corridor can be built out. The risk is not that demand evaporates. It is that demand arrives and finds the quay full and the ferry late.

That is the investment thesis hiding inside the bottleneck. The scarce, high-return assets in this corridor are not the glamorous rail trunk lines that attract sovereign photo-ops; they are the unglamorous links at the water's edge - Caspian vessels, Ro-Ro berths, terminal cranes at Alat and Aktau, and the customs digitisation that the 2026 work plan finally prioritised. Whoever solves the ship shortage captures the margin everyone else is leaving on the table.

What should business and investors watch over the next eighteen months? Three things. First, vessel deliveries - count hulls in the water, not memoranda signed. Second, Anaklia: if Georgian funding stays starved, Black Sea congestion becomes the corridor's permanent ceiling. Third, transit-time reliability, because the corridor wins shippers on predictability, not just geography. Get those three right and the Caucasus owns a trade artery for a generation. Get them wrong and the map stays a map.